From Blitzkrieg to War of Attrition: What the US-Israel-Iran Conflict Reveals

The lesson is not anti-Americanism but realism: Diversify energy sources, fortify domestic buffers, and recalibrate alliances to match 21st-century realities.

|

Listen To This Story

|

Two weeks into the US-Israeli war against Iran — launched on February 28, 2026, under the banner of Operation Epic Fury — the conflict has defied every assumption embedded in Washington’s pre-war planning. What was sold as a rapid decapitation strike, followed by civil unrest and regime change, has instead become a grinding war of attrition that has exposed the physical limits of American power projection.

The material ledger of the fighting, independently modelled by former academic economist Anusar Farooqui – now an independent financial analyst and equities broker based in New York – and corroborated by open-source intelligence and satellite imagery, reveals a theater in which nominal asymmetries in firepower have been neutralized by Iran’s deliberate resource husbandry, distributed command structure, and saturation tactics.

This prelude sets the stage for the first- and second-order economic consequences of Iranian control over the Strait of Hormuz and, ultimately, for the geopolitical recalibrations already underway across the globe and in Asia.

The Material Ledger: Attrition, Depletion, and Timelines

Independent quantitative modelling of drone and missile attrition dynamics provides the clearest window into why the US-led campaign has stalled. The governing equation turns on two rates: the US/Israeli degradation rate of Iranian production and launch facilities and Iran’s reconstitution/repair rate. The critical ratio — namely the repair rate divided by its production and repair rate — determines how long Tehran can sustain high-volume counter-value strikes across the Gulf and maintain closure of the Strait of Hormuz.

Even under conservative assumptions heavily favourable to the US — 90 percent monthly degradation with zero Iranian repair capacity — Iran retains the ability to sustain operationally significant fire for at least four months. In more realistic scenarios, where Iranian repair and rebuild cycles are only modestly impaired, the timeline stretches into six months or longer.

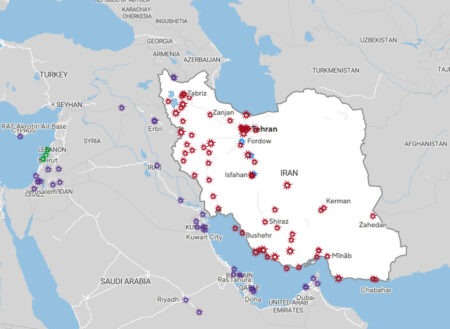

Real-world developments have validated the model’s pessimistic outlook for Washington. In the opening 72–96 hours, Iran deliberately husbanded advanced systems and flooded the zone with older, mass-produced Shahed-style drones and short-range ballistic missiles. The tactic overwhelmed layered air defences: Patriot, THAAD, and allied systems across Bahrain, Qatar, Kuwait, Saudi Arabia, and the UAE. Every single one of the five THAAD batteries deployed in the region has been hit; their AN/TPY-2 radars, among the most sophisticated in the US inventory, have been disabled or destroyed.

Satellite imagery released before commercial providers restricted access over the Gulf shows extensive damage to PAC-3 launchers and associated radar domes. US and Israeli interceptor stocks (SM-3, SM-6, Patriot MIM-104, and THAAD interceptors) are depleting at unsustainable rates. Estimates suggest 35–50 percent degradation in effective US sortie generation capacity, driven by the need to operate from more distant bases after forward facilities were rendered untenable.

The political and military consequences of these strikes have been cascading. Attacks on US bases did not merely degrade infrastructure; they forced a rapid retreat from forward positions. Forces have consolidated at more distant staging areas in the Indian Ocean and eastern Mediterranean, slashing daily sortie rates and necessitating additional aerial refuelling. At least two KC-135 Stratotankers have been downed over western Iraq, with a third damaged. US naval surface groups remain outside effective striking range, deterred by Iran’s layered anti-access/area-denial envelope of coastal missiles, mines, and fast-attack craft.

Early Trump administration claims — broadcast on March 1–2 — that Iranian missile and drone production had been “utterly demolished” were contradicted within days by continued Iranian barrages. Production sites, many distributed and built in underground facilities, have proven far more resilient than anticipated.

Photo credit: CBS / Global Thinkers

The timeline of the conflict to date is instructive.

Days 1–4: saturation strikes deplete interceptor magazines and damage radar infrastructure.

Days 5–9: targeted attacks on US and Gulf-state bases force relocation and expose the fragility of forward basing.

By Day 10, Iranian forces had secured de facto control of the Strait of Hormuz through a combination of direct attacks on commercial shipping, some mine-laying, and selective interdiction. Chinese-flagged tankers continue to transit under negotiated exemptions, while Western and allied shipping has largely halted.

As of March 13 — Day 14 of the war — Iranian production and launch capacity remains operationally intact at 60–70 percent of pre-war levels. US degradation efforts, hampered by the very distance forced upon American aircraft, are running at only 50–65 percent of planned efficiency.

Projecting forward, the material ledger points to a war that could persist for months rather than weeks. Iran’s stockpile of legacy systems, estimated at over 1,500 ballistic missiles and tens of thousands of drones, combined with repair rates that exceed degradation under current US sortie constraints, suggests Tehran can maintain pressure on the strait indefinitely unless Washington commits ground forces and/or accepts dramatically escalated risk to its air and naval assets.

The Trump administration’s outreach via intermediaries (including a reported call to Russian President Vladimir Putin) and quiet Gulf-state soundings toward Tehran reflect recognition of this reality. A decisive US victory — defined as reopening the strait on Washington’s terms and restoring forward basing — now appears improbable within the next 90–120 days.

First-Order Economic Impacts: The Hormuz Chokepoint and Supply Curtailment

Control of the Strait of Hormuz translates directly into leverage over 20 million barrels per day (mbpd) of crude oil and refined products, which is approximately 20 percent of the global supply. Roughly 75–80 percent of this volume is destined for Asian markets. Gas and petrochemical flows, including LNG precursors and chemical feedstocks critical to plastics, fertilisers, and pharmaceuticals, are equally affected. Iran’s selective exemptions for Chinese tankers have prevented total closure but have still produced a net loss of 14–18 mbpd to non-Chinese destinations. The immediate price response has been dramatic: Brent crude has surged toward $180–220 per barrel in spot markets, with forward curves signalling sustained tightness.

Strategic Petroleum Reserve (SPR) releases by the United States, Japan, South Korea, and coordinated International Energy Agency (IEA) members have provided a short-term buffer; roughly 6–7 mbpd at maximum drawdown rates. Yet these reserves were designed for shocks of 5–6 percent supply loss, not 14–20 percent.

American SPR levels are already near 40-year lows; European and Japanese stocks will be exhausted within 30–45 days of sustained release. Historical precedent from Oil Shock 1.0 (1973–79) and the 1990 Gulf War demonstrates how even smaller disruptions (4–6 percent) quadrupled prices or drove Brent from $15 to over $40. A 14–20 percent structural loss, even partially offset, risks $200–250 per barrel peaks if the strait remains contested beyond 60 days.

Photo credit: XindeMaritime / Global Thinkers

Chemical and gas products amplify the shock. The Gulf supplies 30–40 percent of global petrochemical intermediates. Fertilizer prices have risen 80–120 percent in Asian markets, threatening food security in import-dependent economies. LNG spot prices in Asia have doubled, compounding winter heating and industrial energy costs. These first-order effects are not uniform. China’s imports through Hormuz — approximately 6 mbpd pre-war — continue under exemption, while its diversified sourcing (Russia, Central Asia, Africa, Latin America) and domestic buffers absorb the remainder.

Second-Order Impacts: Inflation, Growth, and Supply-Chain Transmission

Beyond headline prices lie deeper transmission mechanisms. In oil-import-dependent Asian economies like Japan, South Korea, the Philippines, Malaysia, Indonesia, Thailand, and Australia, energy costs feed directly into transport, manufacturing, and agriculture. Japan and South Korea, with refining complexes optimised for Middle Eastern crude, face immediate margin compression and export competitiveness erosion.

Diesel and gasoline price spikes of 50–100 percent are already feeding into CPI readings projected to rise 3–5 percentage points in Q2 2026. Southeast Asian manufacturers reliant on diesel for logistics and petrochemicals for plastics see cost increases of 20–40 percent, eroding margins in electronics, textiles and automotive supply chains.

Australia’s dual exposure — LNG export revenues offset by domestic fuel costs — creates fiscal volatility. Second-order effects include currency depreciation (already evident in the won, yen, and rupiah), capital outflows, and tightening monetary conditions that risk tipping fragile post-pandemic recoveries into recession. Fertilizer shortages threaten rice and palm-oil yields across Indonesia, Malaysia, and Thailand, with knock-on food inflation projected at 8–12 percent by mid-year. LNG shortages have led to the shutting of thousands of restaurants in India, and the temporary cessation of fishing by about half of Thailand’s commercial fishing fleet, with flow-on implications for seafood prices domestically and globally.

Western economies face even sharper second-order pain. US gasoline prices approaching $6–8 per gallon and European diesel hikes of €0.50–1.00 per litre threaten to stall consumer spending and industrial output. The International Monetary Fund’s (IMF) historical analysis of 21 countries shows energy shocks transmit 60–80 percent into headline inflation within 6–12 months. With US Treasury deficits already at $1.5 trillion and thin market liquidity, sustained oil prices above $180 risk real-yield spikes, foreign investor retreat (including from China and Japan), and potential market seizures reminiscent of 2022.

China’s Structural Resilience: Buffers, Electrification, and Administrative Levers

China stands in a qualitatively different position, as outlined in my June 2025 analysis “Oil Shock 2.0.” Crude imports have plateaued: 11.1 mbpd peak in 2020, 11.04 mbpd in 2024 (–1.9% yoy). Domestic production stabilises at ~4.3 mbpd through shale and enhanced recovery in Daqing, Tarim, and Bohai basins. Refining capacity exceeds 1 billion tonnes annually, generating a structural export surplus of refined products. Strategic reserves of 1.0–1.2 billion barrels (updated estimates suggest 1.1–1.3 billion with 2025 stockpiling) provide 90–130 days of import cover, far exceeding IEA norms.

Peak diesel demand was recorded in 2024. Electrification of passenger vehicles (over 40 percent of new sales) and expanding industrial electrification, supported by record renewable additions (>300 GW in 2024 alone), have decoupled oil consumption from GDP growth. Oil intensity per unit of GDP continues its secular decline. Coal-to-liquids pathways, while environmentally costly, offer a scalable domestic hedge for diesel and jet fuel in extremis. Administrative pricing, state allocation of fuel to priority sectors (agriculture, logistics and defence), and subsidies financed through state-owned enterprises insulate consumers and industry far more effectively than market-based systems elsewhere.

These structural advantages are reinforced by diplomatic and financial tools. RMB-denominated oil trade via the Shanghai International Energy Exchange has expanded; exemptions for Chinese tankers demonstrate Tehran’s recognition of Beijing’s strategic importance. Even in a worst-case full closure scenario, China’s diversified imports, domestic buffers, and command-economy levers limit headline inflation pass-through to 2–4 percent — half the Western impact — while preserving growth momentum. China is not immune: Higher input costs will pressure certain export sectors and may require targeted fiscal support. But unlike Japan, South Korea or ASEAN importers, Beijing possesses the fiscal capacity, administrative acumen, and energy sovereignty to absorb and redirect the shock.

Geopolitical Fallout: Asian Recalibrations and the Erosion of Extended Deterrence

The material and economic realities are reshaping security calculations from Tokyo to Jakarta. The visible withdrawal of THAAD and Patriot assets from South Korea to replenish Gulf losses has crystallised a new hierarchy of priorities: Persian Gulf contingencies now trump Northeast Asian ones. Seoul, Tokyo, Manila, and Taipei are reassessing the net value of hosting US bases, weapons, and personnel. Once unambiguous security multipliers, these facilities now appear as potential targets in an era of proliferated precision strike. Hosting risks escalation without guaranteed protection, which is a clear inversion of the post-1945 bargain.

Iran’s success in demonstrating the limits of US air-centric power projection accelerates hedging. Japan and South Korea are accelerating LNG diversification, nuclear restarts, and indigenous missile-defense development. Southeast Asian states are deepening Regional Comprehensive Economic Partnership (RCEP) energy cooperation and exploring joint SPR mechanisms. Across the board, the imperative is clear: shorten supply chains, electrify transport fleets, and invest in domestic resilience. The war has made explicit what “Oil Shock 2.0” anticipated — US security guarantees are finite and geographically contingent.

At the heart of this recalibration lies the imperative to shorten vulnerable supply chains, electrify transport fleets at scale, and invest in domestic resilience. China’s advanced electrification trajectory provides both a model and an integrating platform. Having already recorded peak diesel demand in 2024, China sold 16.5 million new energy vehicles (NEVs) in 2025, representing nearly 50 percent of new passenger car registrations and accounting for roughly two-thirds of global EV sales. Battery production reached approximately 770 GWh, a 40 percent increase, with Chinese firms CATL and BYD dominating 69 percent of global installations through LFP technology and rapid charging innovations. Massive renewable additions and administrative tools further reinforce this resilience.

Photo credit: Matti Blume / Wikimedia (CC BY-SA 4.0)

This momentum is rapidly extending across Asia, binding regional electrification more tightly into Chinese supply chains. In Southeast Asia, EV adoption has surged: Thailand and Vietnam now exceed 20–40 percent sales shares, Indonesia 15 percent. These gains are catalyzed by Chinese investments. CATL’s multibillion-dollar battery plants in Indonesia leverage local nickel, while BYD’s factories in Thailand and planned expansions in Malaysia and Vietnam localize assembly. Similar patterns unfold in other markets.

Accelerated electrification is thus reinforcing deeper integration. Under RCEP, preferential terms enable seamless flows of batteries, components, and vehicles. Asian automakers access cost-competitive Chinese technology; Chinese firms secure markets and resources. The result: shorter, resilient chains less exposed to chokepoints.

The war has made explicit what “Oil Shock 2.0” anticipated — US security guarantees are finite and geographically contingent. By embracing electrification anchored in Chinese supply chains, Asia is building a multipolar energy architecture.

Longer term, the conflict accelerates multipolarity. Trump’s impending Beijing visit (March 31–April 2) occurs from a position of demonstrated strategic strain. China, having condemned the war’s initiation while maintaining diplomatic channels, is positioned as a stabilizing actor capable of facilitating de-escalation without offering unilateral concessions. Iran’s campaign to reshape Gulf security — pushing US bases toward drawdown or a full exit — aligns with China’s interest in stable energy flows and the ongoing reduction in dollar dominance for global trade. Gulf monarchies’ quiet outreach to Tehran underscores pragmatic survival over ideological alignment.

In Gramsci’s interregnum, monsters emerge when the old order falters. The Iran war is one such monster: born of overconfidence in legacy doctrines, yet catalyzing the birth of distributed security architectures and economic sovereignty across Asia. The material ledger — depleted interceptors, disabled radars, exhausted forward bases, and sustained Iranian production — has exposed the physical boundaries of American power. The energy shock has laid bare differential vulnerabilities. Asia’s recalculations are already underway: toward electrification, shortened chains, and pragmatic multipolar hedging.

The coming months will determine whether Washington engineers an orderly exit or whether attrition deepens. Either path accelerates the transition already evident since the mid-2010s. American military power retains absolute mass, but its projection now operates within tighter material and political constraints.

For Asian policymakers, the lesson is not anti-Americanism but realism: diversify energy sources, fortify domestic buffers, and recalibrate alliances to match 21st-century realities. In that recalibration lies the foundation for a more balanced, resilient regional order, one in which China’s structural advantages and Asia’s collective agency weigh ever more heavily.

Warwick Powell is an adjunct professor at Queensland University, Australia. He focuses on the intersection of China, digital technologies, supply chains, financial flows, and global political economy & governance. This article was originally published in English and Chinese on Guancha ( Guancha.cn ), a Shanghai-based news site founded in 2012 by Eric X. Li, a venture capitalist and political scientist at Fudan University.