When Will Climate Change Turn Life in the US Upside Down?

Intensifying extreme weather events and an insurance crisis are likely to cause significant economic and political disruption in the US sometime in the next 15 years.

|

Listen To This Story

|

This story by Jeff Masters was originally published by Yale Climate Connections and is part of Covering Climate Now, a global journalism collaboration strengthening coverage of the climate story.

•

The words of explorer John Wesley Powell on the eve of his departure into the unexplored depths of the Grand Canyon in 1869 best describe how I see our path ahead as we brave the unknown rapids of climate change:

We are now ready to start our way down the Great Unknown. We have an unknown distance yet to run, an unknown river to explore. What falls there are, we know not; what rocks beset the channel, we know not; what walls rise over the river, we know not. Ah, well! We may conjecture many things. The men talk as cheerfully as ever; jests are bandied about freely this morning; but to me the cheer is somber and the jests are ghastly.

Powell’s expedition made it through the canyon, but the explorers endured great hardship; suffering near-drownings, the destruction of two of their four boats, and the loss of much of their supplies. In the end, only six of the nine men survived.

Likewise, we find ourselves in an ever-deepening chasm of climate change impacts, forced to run a perilous course through dangerous rapids of unknown ferocity. Our path will be fraught with great peril, and there will be tremendous suffering, great loss of life, and the destruction of much that is precious.

It is inevitable that climate change will stop being a hazy future concern and will someday turn everyday life upside down. Very hard times are coming. At the risk of causing counterproductive climate anxiety and doomism, I offer here some observations and speculations on how the planetary crisis may play out, using my 45 years of experience as a meteorologist, including four years of flying with the Hurricane Hunters and 20 years blogging about extreme weather and climate change. The scenarios that I depict as the most likely are much harsher than what other experts might choose, but I’ve seen repeatedly that uncertainty is not our friend when it comes to climate change. This will be a long and intense ride, but if you stick through the end, I promise there will be a rainbow.

By late this century, I am optimistic that we will have successfully ridden the rapids of the climate crisis, emerging into a new era of non-polluting energy with a stabilizing climate. There are too many talented and dedicated people who understand the problem and are working hard on solutions for us to fail.

Photo credit: Utah Historical Society

What Is a Dangerous Level of Climate Change?

The 1974 made-for-TV movie ‘Hurricane’ included a subplot loosely based on the hurricane party that allegedly occurred during the 1969 landfall of Category 5 Hurricane Camille in Mississippi. The predictable catastrophic end to the party is depicted at the 0:05-second mark of the trailer above. Though the party never happened, legendary TV anchorman Walter Cronkite perpetuated the hurricane party story during one of his broadcasts after the hurricane. As the camera panned over the cement slab littered with debris that marked the former location of the Richelieu Apartments, Cronkite narrated: “This is the site of the Richelieu Apartments in Pass Christian, Mississippi. This is the place where 23 people laughed in the face of death. And where 23 people died.”

Although there is a major climate change hurricane approaching, we’re busy throwing a hurricane party, charging up our planetary credit card to pay for the expenses, with little regard to the approaching storm that is already cutting off our escape routes. This great storm will fundamentally rip at the fabric of society, creating chaos and a crisis likely to last for many decades.

The intensifying climate change storm will soon reach a threshold I think of as a Category 1 hurricane for humanity — when long-term global warming surpasses 1.5 degrees Celsius above preindustrial temperatures, a value increasingly characterized over the last decade as “dangerous” climate change.

For humanity as a whole, this amount of warming is risky, but not devastating. Global warming is currently at about 1.2-1.3 degrees Celsius (2.26-2.23 degrees Fahrenheit) above preindustrial temperatures and is likely to cross the 1.5-degrees Celsius (2.7 degrees Fahrenheit) threshold in the late 2020s or early 2030s.

Assuming that we don’t work exceptionally hard to reduce emissions in the next 10 years, the world is expected to reach 2 degrees Celsius (3.5 degrees Fahrenheit) of warming between 2045 and 2051. In my estimation, that will be akin to a major Category 3 hurricane for humanity — devastating, but not catastrophic.

Allowing global warming to exceed 2.5 degrees Celsius (4.5 degrees Fahrenheit) will cause Category 4-level damage to civilization — approaching the catastrophic level. And warming in excess of 3 degrees Celsius (5.4 degrees Fahrenheit) will likely be a catastrophic Category 5-level superstorm of destruction that will crash civilization.

We must take strong action rapidly to rein in our emissions of heat-trapping gases to avoid that outcome — and build great resilience to the extreme climate of the 21st century that we have so foolishly brought upon ourselves.

According to the Carbon Action Tracker (see tweet below), we are on track for 2.7 degrees Celsius (4.86 degrees Fahrenheit) of warming; if the nations of the world meet their targets for reducing heat-trapping climate pollution, warming will be limited to 2.1 degrees Celsius (3.78 degrees Fahrenheit). There’s a big difference between being hit by a Category 4 versus a Category 3, and every tenth of a degree of warming that we prevent will be critical.

Two years on from Glasgow and our warming estimates for government action have barely moved.

Governments appear oblivious to the extreme events of the past year, somehow thinking treading water will deal with the flood of impacts? https://t.co/fbM4xY9OJe pic.twitter.com/MekGIeU1Z3— ClimateActionTracker (@climateactiontr) December 5, 2023

Climate Change’s Impacts Will Be Highly Asymmetric

As climate scientist Michael Mann explains in his latest book, Our Fragile Moment, great climate science communicator Stephen Schneider once said, “The ‘end of the world’ or ‘good for you’ are the two least likely among the spectrum of potential [climate] outcomes.” So forget sci-fi depictions of planetary apocalypse. That will not be our long-term climate change fate.

But the impacts of climate change will be apocalyptic for many nations and people — particularly those that are not rich and white. People and communities with the least resources tend to be the first and hardest hit by climate change, not only because poorer people and communities are inherently more vulnerable to the impacts of any disaster, but also because the extremes induced by climate change tend to be worse in the tropics and subtropics, home to many poor nations.

In the US, climate change has already turned life upside down for numerous communities. For example, in North Carolina, the financially strapped, Black-majority towns of Fair Bluff and Princeville are in danger of abandonment from hurricane-related flooding (from Hurricane Floyd in 1999, Matthew in 2016, and Florence in 2018). Seven Springs, NC (population 207 in 1960, now just 55) is largely abandoned.

Climate change was a key contributor to these floods; a 2021 study found that about one-third of the cost of major US flood events since 1988, totaling $79 billion, could be attributed to climate change. And for the town of Paradise, CA — utterly destroyed by the devastating Camp Fire of 2018, which killed 85 and caused over $16 billion in damage — climate change has been apocalyptic.

An Immediate US Climate Change Threat: An Insurance Crisis

In the US, the most likely major economic disruption from climate change over the next few years might well be a collapse of the housing market in flood-prone and wildfire-prone states. Billion-dollar weather disasters — which cause about 76 percent of all weather-related damages — have steadily increased in number and expense in recent years and would be even worse were it not for improved weather forecasts and better building codes. The recent increase in weather-disaster losses has brought on an insurance crisis — especially in Florida, Louisiana, California, and Texas — which threatens one of the bedrocks of the US economy, the housing and real estate market.

In California, the insurer of last resort, the FAIR plan, had only about $250 million in cash on hand as of March 2024.

“One major fire near Lake Arrowhead, where the Plan holds $8 billion in policies, would plunge the whole scheme into insolvency,” observed Harvard’s Susan Crawford, author of Charleston: Race, Water, and the Coming Storm.

It is widely acknowledged that higher weather disaster losses result primarily from an increase in exposure: more people with more stuff moving into vulnerable places, including those at risk of floods. Martin Bertogg, Swiss Re’s head of catastrophic peril, said in a 2022 AP interview that two-thirds, perhaps more, of the recent rise in weather-related disaster losses is the result of more people and things in harm’s way.

But this balance will likely shift in the coming decades. Increased exposure will continue to drive increased weather disaster losses, but the fractional contribution of climate change to disaster losses — at least for wildfire, hurricane, and flood disasters — is likely to increase rapidly, making the insurance crisis accelerate.

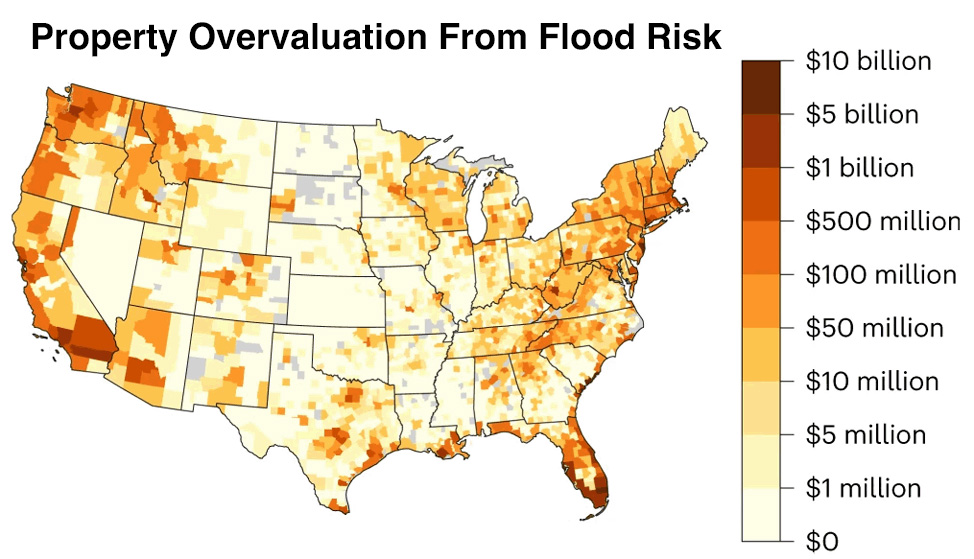

Photo credit: Gourevitch et al., 2023, Unpriced climate risk and the potential consequences of overvaluation in US housing markets, “Nature Climate Change” volume 13, pages 250–257.

A 2023 study (Fig. 2) drew attention to a massive real estate bubble in the US: the vast number of properties whose purported value doesn’t account for the true costs of floods. The study estimated that across the US, residential properties are overvalued by a total of $121-237 billion under current flood risks. This bubble will likely continue to grow as sea levels rise, storms dump heavier rains, and unwise risky development continues.

Likewise, US properties at risk of wildfires are collectively overvalued by about $317 billion, according to David Burt, a financial guru who foresaw the 2008 subprime mortgage crisis. Insurers are already pulling out of the areas most at risk, threatening to make property ownership too expensive for millions and posing a serious threat to the economically critical real estate industry.

Climate futurist Alex Steffen has described the climate change-worsened real estate bubble this way:

As awareness of risk grows, the financial value of risky places drops. Where meeting that risk is more expensive than decision-makers think a place is worth, it simply won’t be defended. It will be unofficially abandoned. That will then create more problems. Bonds for big projects, loans, and mortgages, business investment, insurance, talented workers — all will grow more scarce. Then, value will crash, a phenomenon I call the Brittleness Bubble.

Something brittle is prone to a sudden, catastrophic failure and cannot easily be repaired once broken. The popping of the real estate Brittleness Bubble will potentially trigger panic selling and a housing market collapse like a miniature version of the Great Financial Crisis of 2008 but focused on the 20 percent of American homes in wildfire and flood risk zones. In his 2023 Congressional testimony, Burt estimated that a wildfire and flood-induced repricing of risk of the US housing market could have a quarter to half the impact of the 2008 Great Financial Crisis.

However, the 2008 crisis was relatively short-lived, as fixes to the financial system and a massive federal bailout led to a rebound in property values after a few years. A climate change-induced housing crisis will likely be resistant to a similar fix because the underlying cause will worsen: Sea levels will continue to rise, flooding heavy rains will intensify, and wildfires will grow more severe, increasing risk.

Science writer Eugene Linden wrote in 2023, “As we saw in 2008, a housing crisis can quickly morph into a systemic financial crisis because banks own most of the value, and thus the risk, in housing and commercial real estate.”

Crawford of Harvard recently wrote: “Because insurance can help communities and households recover more quickly from disasters, and because so much of the US economy is driven by spending on housing, the inaccessibility and unaffordability of insurance poses a threat to the stability of the entire economy.”

As Sen. Sheldon Whitehouse, a Democrat from Rhode Island, said earlier this year, “The thing about economic crises is that they come on slowly, until they come on fast.”

How the Insurance Crisis May Play Out: The “Wholly Irrational and Completely Ad-Hoc Pirate Capitalism” Solution

In his blunt 2023 essay, “Insurance Politics at the End of the World,” journalist Hamilton Nolan offers these thoughts on the potential ways this climate change-induced insurance crisis could be addressed:

The rational capitalism solution here is: We accurately price your risk and that risk becomes unaffordable and people move away from areas that are stupid to live in and therefore climate adaptation is achieved. The rational socialism solution is: We collectively embrace the idea that we need to adapt to climate change and the federal government creates long-term programs that incentivize moving away from areas that are stupid to live in and disincentivize “build as much crap in South Florida flood zones as you can now to take advantage of the real estate bubble” and generally cushion the economic blow for all the people whose lives will have to change.

The path we are on today, though — the path that our current political system makes likely — is the path of Wholly Irrational and Completely Ad-Hoc Pirate Capitalism: Increasing climate change-induced disasters cause panic among homeowners as a class; politicians rush to grab dollars to enable everyone to live the same as they are now for as long as possible; and eventually the whole thing crashes into the wall of reality in a way that causes uncontainable, national pain rather than just the specific, regional, temporary pain of the smarter solutions.

When Will the Brittleness Bubble Pop?

When might this “crash into the wall of reality” happen and the Brittleness Bubble pop? Politicians are working extremely hard to keep their jobs by delaying this day of reckoning, artificially limiting insurance rate rises, and offering state-run insurance plans of last resort. This approach — the equivalent of giving a blood transfusion to the injured, without stopping the bleeding — does not fix the underlying problem and all but guarantees that the pain of the eventual national reckoning will be much larger. Insurance is designed to transfer risk, but risk is rising everywhere.

As the hurricane season is set to begin soon and wildfire risk gradually increasing, private insurers in some states are fleeing areas considered at high risk.

It's leaving so-called "residual," or last resort plans, to pick up the tab. https://t.co/3sxv9m0FOS pic.twitter.com/YTkZ9OlJE3

— Axios (@axios) May 10, 2024

Crawford addressed the issue in a 2024 essay, “Who ends up holding the bag when risky real estate markets collapse?” Citing financial guru Burt, she concluded: “2025 or 2026 is when things give way and it becomes very difficult to offload houses and buildings in risky places where mortgages are suddenly hard to get, much less insurance.” When asked in an interview with Marketplace if the market is due for another correction, as homeowners in places with growing risk of flooding and wildfire have to pay more for insurance, Burt said:

This is actually happening right now and is probably going to happen over the next three to five years, like a full reckoning of these new costs for 15 or 20 percent of the homes in the US … If all their equity is already gone [because of lowered property values], their costs are going up a ton, they can barely afford it, that’s when people walk away.

In the same Marketplace story, though, Ben Keys, a professor of real estate and finance at the University of Pennsylvania’s Wharton School, said, “The idea that we would expect there to be a huge wave of defaults or delinquencies feels relatively unlikely.”

But like Burt, climate change futurist Steffen predicts the real estate Brittleness Bubble will pop within five years (10 at the most).

I suspect we're less than 5 years away from a prolonged surge of value loss in real estate assets based on risk, insurability, economic brittleness and local capacities to ruggedize (or not).

That kind of devaluation will echo through the whole economy.https://t.co/Qs0zyMS38g

— Alex Steffen (@AlexSteffen) May 21, 2024

This reckoning could come sooner for Florida if another $100 billion hurricane hits. The Florida insurance and coastal property market did manage to withstand the $117 billion cost of Category 4 Hurricane Ian of 2022, but another blow like that might well cause a severe downward spiral in the Florida real estate market from which it might never fully recover. This vulnerability was underscored by Florida Gov. DeSantis during a 2023 radio interview with a Boston host, when DeSantis suggested homeowners should “knock on wood” and hope the state didn’t get hit by a hurricane in 2024.

But “knocking on wood” is not an effective climate adaptation strategy for Florida. Because of climate change, Mother Nature is now able to whip heavier bowling balls with more devastating impact down Hurricane Alley. It’s only a matter of time before she hurls a strike into a major Florida city, causing an intensified coastal real estate and insurance crisis. And the odds of such a strike are higher than average in 2024 because of record-warm ocean temperatures in the tropical Atlantic, combined with a developing La Niña event.

Like this hyper-strike rolling robot, Mother Nature is now able to whip heavier bowling balls with more devastating impact down hurricane alley because of the extra heat energy in the oceans from human-caused global warming.

Watch Out for Increased Coastal Flooding in the Mid-2030s

We may manage to avoid a coastal real estate market crash in the next 10 years if we get lucky with hurricanes and if our politicians continue to pump huge amounts of money to bail out the failing system.

But it will become increasingly difficult to keep the coastal property market propped up beginning in the mid-2030s because of accelerating sea-level rise combined with an 18.6-year wobble in the moon’s orbit. Thus, I expect that the longest we might stave off the popping of the coastal real estate Brittleness Bubble is 15 years.

Photo credit: NASA sea-level rise tool

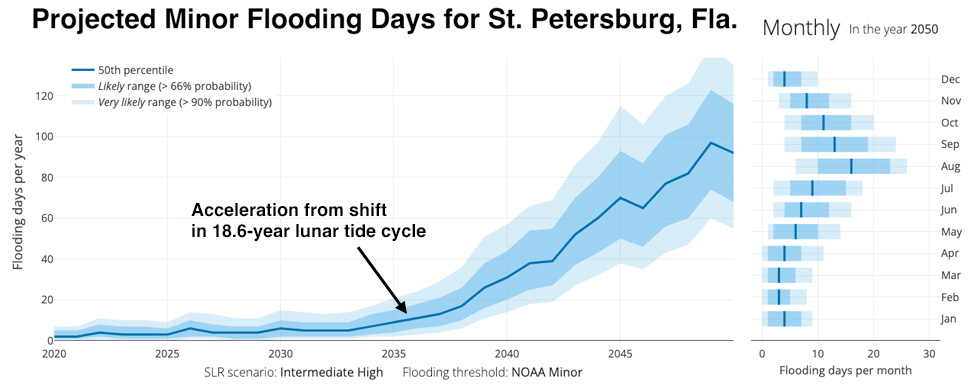

As I wrote in my 2023 post, “30 great tools to determine your flood risk in the US,” beginning in 2033, the moon will be in a position favorable for bringing higher tides to locations where one high tide and low tide per day dominate. This will bring a rapid increase in high tide flooding to the coasts of the Gulf of Mexico, the Southeast, the West Coast, and Hawaii. This expected acceleration in the mid-2030s is obvious for St. Petersburg (Fig. 3), plotted using NASA’s Flooding Analysis Tool and Flooding Days Projection Tool. The rapid acceleration in coastal flooding simultaneously along a huge swathe of heavily developed US coast in the mid-2030s will be sure to significantly stress the coastal housing market. And according to the Coastal Flood Resilience Project, the nation is flying blind on the possible impacts: There are no national assessments of the potential loss of major, critical infrastructure assets to coastal storms and rising seas.

A Second Potential Immediate US Climate Change Threat: A Global Food Shock

Another immediate danger: a series of global extreme weather events affecting agriculture, causing global economic turmoil.

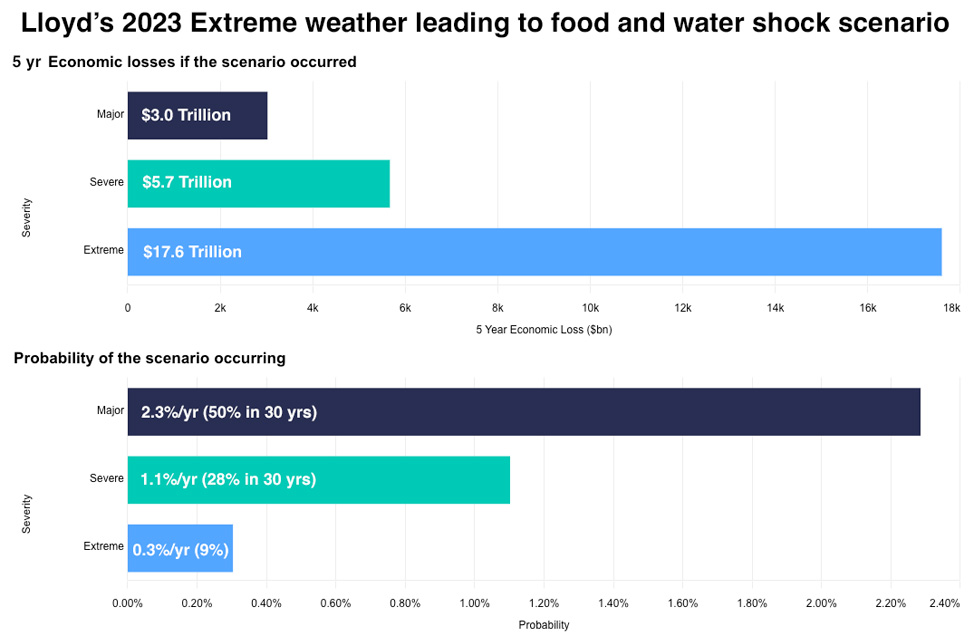

In my 2024 post, “What are the odds that extreme weather will lead to a global food shock?” I reviewed a 2023 report by insurance giant Lloyd’s, which modeled the odds of a globally disruptive extreme food shock event bringing simultaneous droughts in key global food-growing breadbaskets. The authors estimated that a “major” food shock scenario costing $3 trillion globally over a five-year period had a 2.3 percent chance of happening per year (Fig. 4). Over a 30-year period, those odds equate to about a 50 percent probability of occurrence — assuming the risks are not increasing each year, which, in fact, they are.

Photo credit: Lloyds

“Black Swan” and “Gray Swan” Extreme Weather Events

Yet another concern for the US is the risk of wholly unanticipated “black swan” extreme weather events that scientists didn’t see coming. As Harvard climate scientists Paul Epstein and James McCarthy wrote in a 2004 paper, “Assessing Climate Instability”: “We are already observing signs of instability within the climate system. There is no assurance that the rate of greenhouse gas buildup will not force the system to oscillate erratically and yield significant and punishing surprises.”

One example of such a punishing surprise was Superstorm Sandy of 2012, that unholy hybrid spawn of a Caribbean hurricane/extratropical storm that became the largest hurricane ever observed and one of the most damaging, costing $88 billion. And who anticipated that a siege of climate-change-intensified wildfires in western North America beginning in 2017, causing multiple summers of horrific air quality that would significantly degrade the quality of life in the West? Or the jet stream experiencing a sudden increase in unusually extreme configurations over the past 20 years, leading to prolonged periods of intense extreme weather over multiple portions of the globe simultaneously? As the late climate scientist Wally Broecker once said, “Climate is an angry beast, and we are poking at it with sticks.”

Just as concerning might be future “gray swan” events — extreme weather events that climate models anticipate could happen but exceed anything in the historical record. (“Gray swan” is an expression first coined by hurricane scientist Kerry Emanuel in his 2016 paper, “Grey swan tropical cyclones.”) Several potential gray swan events I have written about include a $1 trillion California “ARkStorm” flood, the potential failure of the Old River Control Structure during an extreme flood that allows the Mississippi River to change course, or a storm like 2015’s Hurricane Patricia, with winds over 200 mph, hitting Miami, Galveston/Houston, Tampa, or New Orleans. The risk of gray swan events is steadily increasing.

A ‘New Normal’ of Extreme Weather Has Not Yet Arrived

I’m often asked if the absurdly extreme weather events we’ve been experiencing recently are the new normal. “No!” I reply. “Heat is energy, so the energy to fuel more intense extreme weather events will increase until we reach net-zero emissions. At that time the climate will finally stabilize at a new normal with a highly dangerous level of extreme weather events.”

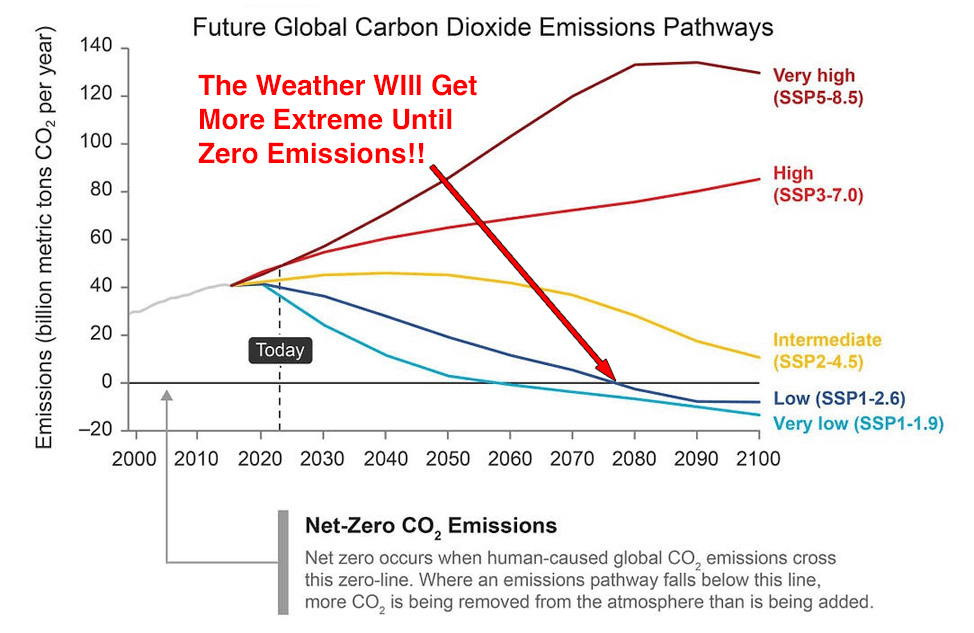

Barring a series of extraordinary volcanic eruptions or a major geoengineering effort, even under an optimistic “low” emissions climate scenario, the earliest the climate might stabilize is in the mid-2070s (Fig. 5); thus the weather will grow more extreme, on average, for at least the next 50 years. Considering that CO2 emissions have not yet peaked and may be following the “intermediate” pathway shown below, there is considerable danger that the weather will still be growing more extreme when today’s children are very old early next century. But even when net-zero emissions are reached, sea-level rise will continue to occur at a pace difficult to adapt to, and the climate crisis will continue to intensify.

Photo credit: 2023 U.S. National Climate Assessment, with annotation added

Longer-Range Concerns: Global Catastrophic Risk Events

The high probability that the weather will grow more extreme throughout the lifetime of everybody reading this essay means that we have to take seriously some very bad long-term threats. As I wrote in my 2022 post, “The future of global catastrophic risk events from climate change,” a global catastrophic risk event is defined as a catastrophe global in impact that kills over 10 million people or causes over $10 trillion (2022 USD) in damage. Since the beginning of the 20th century, there have been only three such events: World War I, World War II, and the COVID-19 pandemic. But climate change is a threat multiplier, increasing the risk of five types of global catastrophic risk events:

- Drought

- War

- Coastal flooding from sea-level rise and land subsidence

- Pandemics

- Collapse of the Atlantic Meridional Overturning Circulation (AMOC), the powerful currents that circulate warm water in the tropical Atlantic Ocean to the Arctic and back (an August 2024 study gave a 59 percent chance of an AMOC collapse occurring before 2050)

The likeliest of these is a global catastrophic risk event from sea-level rise, which is highly likely to occur by the end of the century. For example, a moderate global warming scenario will put $7.9-12.7 trillion dollars of global coastal assets at risk of flooding from sea-level rise by 2100, according to a 2020 study: “Projections of global-scale extreme sea levels and resulting episodic coastal flooding over the 21st century.” Although this study did not take into account assets that inevitably will be protected by new coastal defenses, neither did it consider the indirect costs of sea-level rise from increased storm surge damage, mass migration away from the coast, increased saltiness of fresh water supplies, and many other factors. A 2019 report by the Global Commission on Adaptation estimated that sea-level rise will lead to damages of more than $1 trillion per year globally by 2050.

Furthermore, sea-level rise, combined with other stressors, might bring about megacity collapse — a frightening possibility when infrastructure destruction, salinification of freshwater resources, and a real estate collapse potentially combine to create a mass exodus of people from a major city, reducing its tax base to the point that it can no longer provide basic services. The collapse of even one megacity might have severe impacts on the global economy, creating increased chances of a cascade of global catastrophic risk events. One megacity potentially at risk of this fate is the capital of Indonesia, Jakarta, with a population of 10 million. Land subsidence of up to 2 inches per year and sea-level rise of about an eighth of an inch per year are causing so much flooding in Jakarta that Indonesia is constructing a new capital city in Borneo.

https://twitter.com/rahmstorf/status/1778444205234258364

I also expect one or more climate change-amplified global catastrophic risk events from drought will occur this century. Mexico City, with a metro area population of 22 million, has suffered record heat over the past year, is in danger of its reservoirs running dry, and is drilling ever-deeper wells to tap an overtaxed aquifer. Though the city will muddle through the crisis now that the summer rains have come this year, what is the plan for 30 years from now, when the climate is expected to be drier and much, much hotter? Although Mexico City can greatly improve its water situation by fixing a poorly maintained system that has a 40 percent loss rate, it is unclear how the city will be able to survive the much hotter and drier climate of 30 years from now. And at least 10 other major cities are in a similar bind.

Technology can help us adapt to a hotter climate by providing air conditioning (if you are rich enough), but technological solutions to create more water availability when the taps run dry are much more difficult to achieve. I believe water shortages will drive a partial collapse of and mass migration out of multiple major cities 20-40 years from now, significantly amplifying global political and economic turmoil. For example, a 2010 study, “Linkages among climate change, crop yields and Mexico-US cross-border migration,” found that a 10 percent reduction in crop yields in Mexico leads to an additional 2 percent of the population emigrating to the United States.

In his frightening 2019 book Food or War, science writer Julian Cribb documents 25 food conflicts that have led to famine, war, and the deaths of more than a million people — mostly caused by drought. Since 1960, Cribb says, 40-60 percent of armed conflicts have been linked to resource scarcity, and 80 percent of major armed conflicts occurred in vulnerable dry ecosystems. Hungry people are not peaceful people, Cribb argues.

Devastating Impacts From Climate Change Are Accelerating

Though climate change itself is not accelerating faster than what climate scientists and climate models predicted, devastating impacts from climate change do seem to be accelerating. That is because the new climate is crossing thresholds beyond which an infrastructure designed for the 20th century can withstand. These breaches are occurring in tandem with an increase in exposure — more people with more stuff living in harm’s way — which is the dominant cause of the sharp increase in weather-disaster losses in recent years. It’s sobering to realize that the current US insurance crisis has primarily been driven by increased exposure and foolish insurance policies that promote development in risky places — not climate change — and that climate change’s relative contribution to the crisis is set to grow significantly.

Accelerating sea-level rise alone is sure to cause a massive shock to the US economy; according to a 2022 report from NOAA, sea level along the US coastline is projected to rise, on average, 10-12 inches (0.25-0.30 meters) in the next 30 years (2020-2050), which will be as much as the rise measured over the last 100 years (1920-2020). At this level, 13.6 million homes might be at risk of flooding by 2051, triggering a mass migration of millions of people away from the coast.

If we add to sea-level-rise-induced migration the additional migration that will result from climate change-intensified wildfires, heat waves, and hurricanes, we are forced to acknowledge the reality that a nation-challenging Hurricane Katrina-level climate change storm has already begun in the US, one which has the potential to cause catastrophic damage. As I wrote in my June post “The US is finally making serious efforts to adapt to climate change,” there have been some encouraging efforts to prepare for the coming mass migration. But, as I argued in my follow-up post “The US is nowhere near ready for climate change,” we remain woefully unprepared for what is coming.

And my subsequent post “Can a colossal extreme weather event galvanize action on the climate crisis?” argues that we should not expect that any future extreme weather event or breakdown of the climate system will galvanize the type of response needed — we’ve already had at least 13 events since 1988 that should have done so, yet have not. Even if such an event did prompt strong, transformative change, it’s too late to avoid having life turned upside-down by climate change. It’s like we’ve waited until our skin started getting red before seeking shade from the sun, and we’re only now taking our first stumbling steps toward shade. Well, it’s a long hike to shade, and a blistering sunburn is unavoidable.

Given the unprecedented nature and complexity of this planetary crisis, there is huge uncertainty on how this drama may unfold; there are climate scientists who offer a more optimistic outlook than I do (for example, Hannah Ritchie, author of Not the End of the World’), and those who are more pessimistic (James Hansen).

I suggest that you make the most of the current “calm before the storm” and prepare for the chaotic times ahead, which could begin at any time. I will offer my recommendations on how to do this in my next post in this series, “What should you do to prepare for the climate change storm?”

Paleolithic Emotions, Medieval Institutions, and Godlike Technology

The urgency to rapidly deal with the climate crisis was succinctly summarized by the Intergovernmental Panel on Climate Change in its latest summary report: “There is a rapidly closing window of opportunity to secure a livable and sustainable future for all.”

But taking advantage of that window of opportunity is difficult because of human psychological and political realities. In climate scientist Peter Gleick’s 2023 book, The Three Ages of Water, he quotes Harvard’s E.O. Wilson, father of sociobiology, who perhaps said it best: “The real problem of humanity is the following: We have Paleolithic emotions, medieval institutions, and godlike technology. And it is terrifically dangerous, and it is now approaching a point of crisis overall.”

The boat of civilization has already hit multiple rocks along the rapids of climate change and is taking on water. Perilous rapids with even more dangerous rocks and waterfalls lie before us, but the course of our boat cannot be so easily altered to avoid the rocks, because of our Paleolithic emotions and medieval institutions. As a result, we may have only a few more years — or perhaps as long as 15 years — of relative normalcy in our everyday lives here in the US before the approaching climate change storm ends our golden age of prosperity. But this “golden age” was made of fool’s gold, paid for with wealth plundered from future generations.

Hope for the Future Via ‘Cathedral Thinking’

Though this essay has dwelt on some grim realities, I am optimistic that we will prevent climate change from becoming a civilization-destroying category 5-level catastrophe. But we must fight extremely hard to correct the course of our boat and not allow its inertia to carry us into the rocks that stud the rapids of climate change. This is not a task that can be accomplished in our lifetimes.

Photo credit: Walwyn / Flickr (CC BY-NC 2.0 DEED)

Susan Joy Hassol, the climate communication veteran who served as a senior science writer on three National Climate Assessments, put it this way in an interview with Yale Climate Connections contributor Daisy Simmons: “This is the fight of our lives, and it’s a multigenerational task. We need what’s been called ‘cathedral thinking.’ That is, the people who started working on that stone foundation, they never saw the thing finished. It took generations to get these major works done. This is that kind of problem. And we have to all do our part. The more I act, the better I feel, because I know I’m part of the solution.”

Actions we take now will yield enormous future benefits, and the faster we undertake transformative actions to adapt to the new climate reality, the less suffering will occur. The Global Commission on Adaptation says that “every $1 invested in adaptation could yield up to $10 in net economic benefits, depending on the activity.” We should work to build our cathedral of the future with the thought that each action we take now will multiply by a factor of 10 in importance in the future.

An excellent @nytimes article on rapid growth of wind, solar, & EVs, including factories, in the US. Costs are below fossil and nuclear (see graphs). Reasons why, graphs with how fast, pictures of it happening. https://t.co/uglQDnE97t pic.twitter.com/oIpLmlp28v

— Willett Kempton (@WillettKempton) September 5, 2023

But some of the hardest work has been done: The cornerstone of this cathedral of the future has already been laid. The clean energy revolution is here and has progressed far more rapidly than I had dared hope. Passage of the 2021 Bipartisan Infrastructure Law and 2023 Inflation Reduction Act has been instrumental in getting this cornerstone laid. Solar energy is now the cheapest source of energy in world history and the costs of wind power and battery technology have also plummeted. Two recent reports were optimistic that climate-warming carbon dioxide emissions had finally peaked in 2023, and GDP growth has decoupled from carbon dioxide emissions in recent years, giving hope that economic growth can still occur without making the planet hotter.

At its heart, the root of the climate crisis is humanity’s spiritual inharmoniousness: We overvalue the pursuit of material wealth and we worship billionaires but undervalue growing more connected to our spiritual selves and acting to preserve and appreciate the natural systems that sustain us. Making yourself more peaceful and loving through quiet spiritual pursuits and time spent in nature will help counteract the anxiety and fear sparked by the climate crisis. But in tandem with your increased peace must come a righteous anger to “throw the money changers out of the temple” and topple the might of the fossil fuel industry and its enablers.

So put your shoulder to an oar! Help us power the boat of civilization through the rapids of climate change. All of humanity shares the same boat, and you have the opportunity to make your own unique and valuable contribution to the effort.

This is a nice way to visualize the pathway to your unique climate action. https://t.co/cjlv5XXrak

— Jeff Masters (@DrJeffMasters) May 15, 2024

As promised, here is the rainbow at the end. It’s the intro image from my first and last Weather Underground blog posts, “The 360-degree Rainbow” and “So long, wunderground!” My unique and valuable contribution to building our new cathedral has not yet reached the end of the rainbow for a rainbow has no end — it is a full circle. One just has to fly high in a rainstorm where the sun is shining to see it.

Photo credit: Jeff Masters / NOAA

I will continue to make my voice heard as long as climate science-denying politicians, corporations, media pundits, and wealthy individuals continue to row the boat of civilization into the rocks of climate-change catastrophe. I encourage those of you who have learned about extreme weather and climate change from me to do the same. To get started, learn from one of the best communicators in the business, climate scientist Katherine Hayhoe:

Recommended reading:

- What should you do to prepare for the climate change storm?

- Can a colossal extreme weather event galvanize action on the climate crisis?

- The US is nowhere near ready for climate change

- The US is finally making serious efforts to adapt to climate change

- Book review: On the Move is a must-read account of US climate migration

- Book review: The Great Displacement is a must-read

- Part one of my three-part sea-level rise series: How fast are the seas rising?

- Part two of my three-part sea-level rise series: Eight excellent books on sea-level rise risk for US cities

- Part three of my three-part sea-level rise series: 30 great tools to determine your flood risk in the US

- Bubble trouble: Climate change is creating a huge and growing US real estate bubble

- Many coastal residents willing to relocate in the face of sea-level rise

- Disasterology: a book review

- The future of global catastrophic risk events from climate change

- With global warming of just 1.2 C, why has the weather gotten so extreme?

- Recklessness defined: breaking 6 of 9 planetary boundaries of safety

- Retreat From a Rising Sea: A book review

- Quick facts on climate change, extreme weather-related events, and their impacts on society

- Susan Crawford’s substack feed on climate adaptation policy, Moving Day

- Climate futurist Alex Steffen’s newsletter

Susan Joy Hassol (@ClimateComms) and Bob Henson (@bhensonweather) provided helpful edits for this post.

•

![]()